Testimony to the House Government Operations Committee Regarding Act H.397

Testimony to the House Government Operations Committee

Regarding Flood-Related Municipal Financing (H.397)

Josh Hanford, Director of Intergovernmental Affairs, VLCT

March 14, 2025

Good Government: VLCT/VBB Suggested Amendments Related to Municipal Finance

Given the various unique charter authorities in some communities, these provisions are most likely to help rural towns.

These proposal have been broadly socialized across the legislature this session and are well received. Other committees where we have testified include Senate Appropriations, Senate Government Operations, House and Senate Transportation.

They are supported by VLCT, Vermont Bond Bank, Clerks and Treasurers, School Business Officials, and Governmental Finance Officials and UAFB is recommended by numerous auditors.

All together, these provisions will improve emergency responsiveness for municipalities, create new, stabilizing factors for local property taxes, and will improve grant readiness for towns and cities as we approach a potentially volatile period for federal funding.

July 10,2024 Municipal Flood Damages

Examples of outstanding emergency debt pending FEMA reimbursement:

Lyndon: $15M (x2 the town budget)

Moretown: $8.25M

Middlesex: $7M (x3 the town budget)

Cavendish $1.6M

Barnet: $1.5M

Bridgewater: $3M (2x the town budget)

Of the municipal entities impacted by July 2024 severe storm, one third (1/3) make up 91% of the total estimated damages.

Two thirds (2/3) of the municipalities impacted were also impacted in July 2023.

Of these towns that were impacted in both years

64% are towns with less than 2000 population

82% are towns with less than 5000 population

Unassigned Fund Balance

We recommend action to allow municipalities to employ the prudent fiscal practice of providing for unassigned fund balance within the municipal general fund budget.

An Unassigned Fund Balance, sometimes called a “rainy day fund”, is simply the difference between assets and liabilities.

Establishing an Unassigned Fund Balance would assist in cash flow management, stabilize the tax rate, improve emergency response, and significantly strengthen their financial resiliency in the case of unexpected negative economic trends

A strong Unassigned Fund Balance improves grant readiness by making flexible monies available for local matches when grant opportunities arise and improves the municipality's borrowing position, saving taxpayers money on the cost of municipal debt.

Emergency Borrowing

VLCT and the Vermont Bond Bank request a new authority to borrow for up to a five-year repayment period in the case of an all-hazards event.

Vermont municipalities have become increasingly familiar with complex and extensive processes required to access emergency funding and FEMA Public Assistance.

In the wake of flooding and major weather events, municipalities cannot wait to rebuild vital town infrastructure or to restore municipal services.

State law substantially limits the authority of local legislative bodies to acquire funding for emergency response as they can only take on debt for up to one year without a town vote.

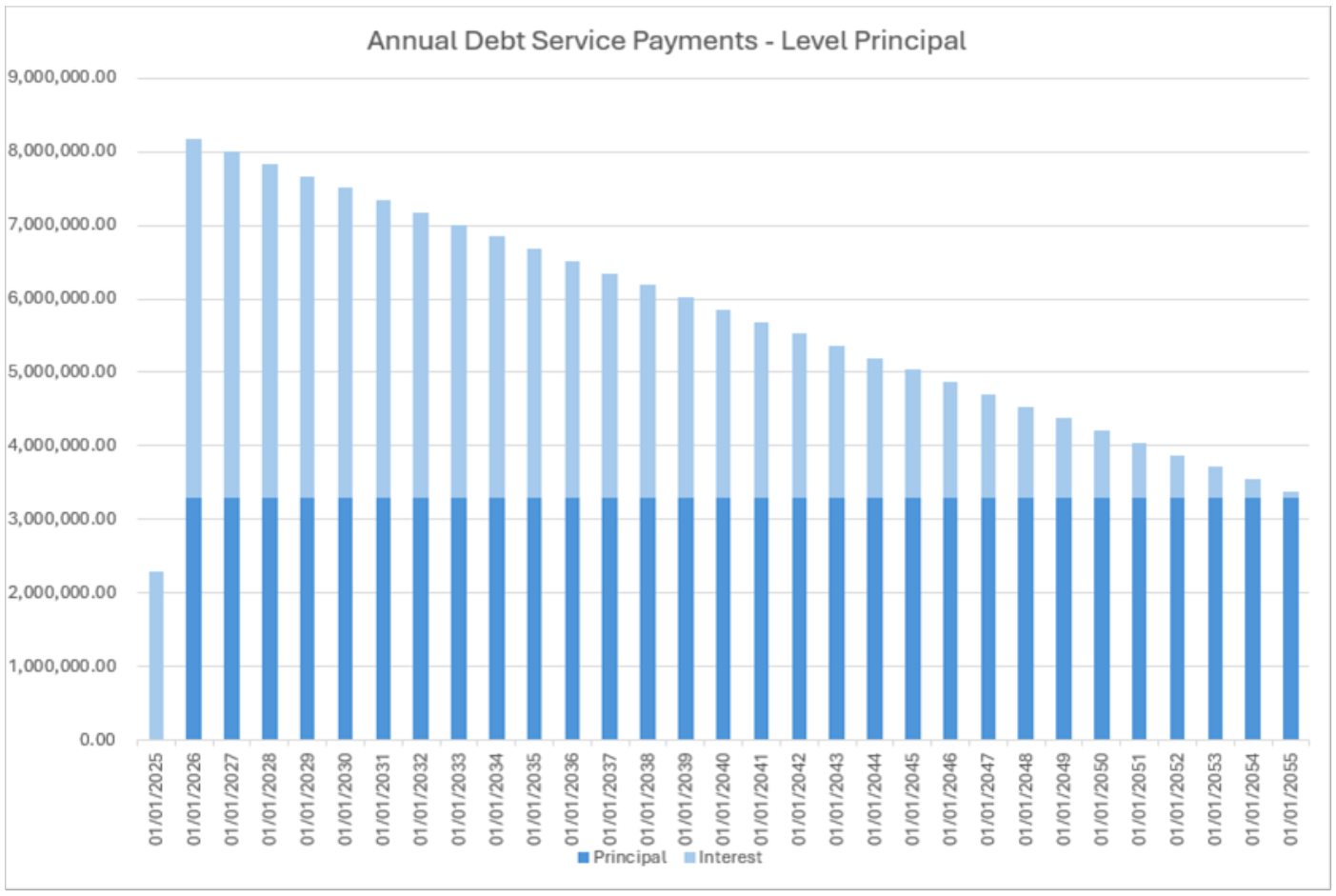

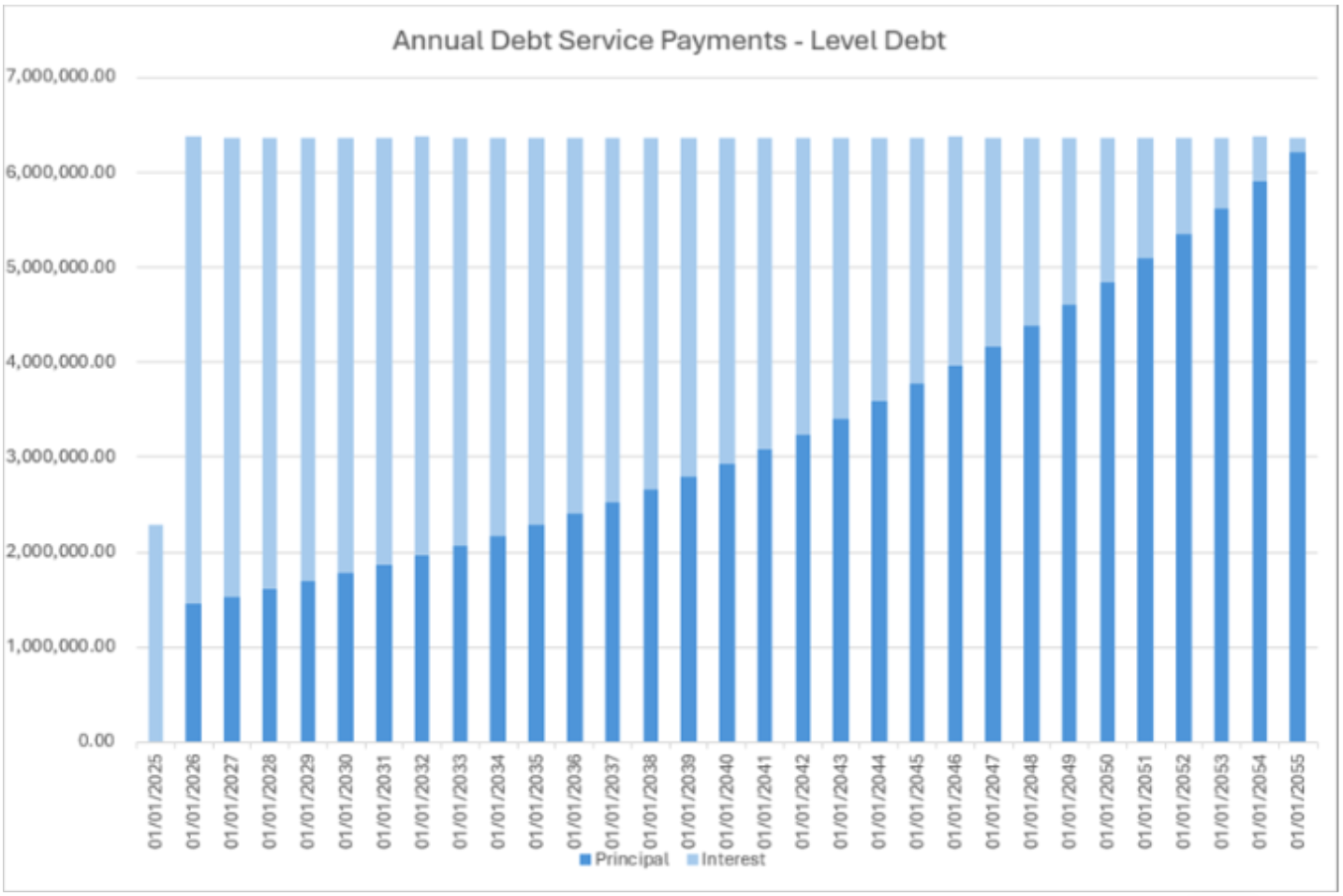

Level Debt Service

To improve predictability for municipalities and for taxpayers, VLCT and the Vermont Bond Bank request a change to allow for flexibility in bond repayments to include level debt option. Members of the Vermont School Board Association and Superintendents Associations have also expressed support for this change.

Current statute requires municipal loans to be level principal.

Debt payments for level principle borrowings start high and decrease yearly as the cost of interest goes down.

Municipalities should have the option to structure level debt or level principle.

This is more within the norms of government borrowing nationally.

Approaches to Funding Flood Resiliency

Financing strategies must be paired with appropriate technical assistance for grants management and municipal finance, and with expanded municipal authorities to exercise best practices for government finance.

Grants are competitive and require local matches.

FEMA reimbursement is complex and time consuming.

In addition to stormwater districts, consider tax increment financing.

*NEW* Our Municipal Operations Support Team is funded by a $1 million USDA Rural Development grant to assist local officials with financial management, grant funding, ARPA, project development, and more .

VLCT supports and appreciates legislative action to expand municipal authorities, increase investment, and create new resources for improved emergency management and flood resiliency

For elements of the proposals (relating emergency management and buy outs in particular) consider "all-hazard event" vs. "all hazards flood event".

Ensure ongoing funding for the state flood impacted property buyout program.

Include support for the relocation of threatened municipal buildings.

Consider grant list impacts.