These FAQs were developed based on questions from members. If you don't find what you're looking for here, please take a look at our Compliance and Reporting page or the main ARPA webpage. If you need more assistance please email arpa@vlct.org.

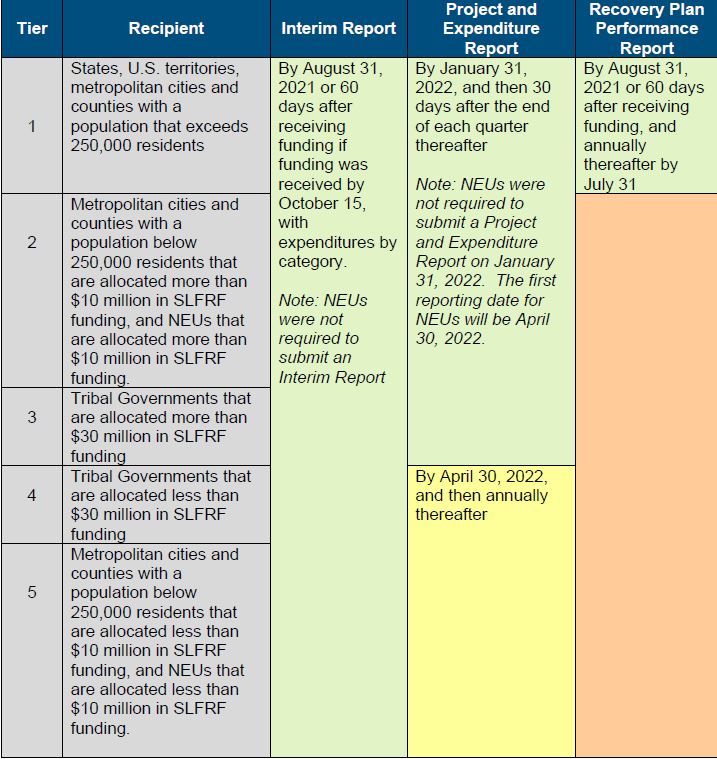

The Authorized Representative for Reporting is responsible for certifying and submitting official reports on behalf of the SLFRF/ARPA recipient. Treasury will accept reports or other official communications only when submitted by the Authorized Representative for Reporting. The Authorized Representative for Reporting is also responsible for communications with Treasury on such matters as extension requests and amendments of previously submitted reports. The official reports may include special reports, quarterly or annual reports, interim reports, and final reports.

The "Date of Award" is the date your town/city/village certified to accept its ARPA funding (summer 2021).

Certain federal regulations are applicable to your ARPA award, such as Uniform Guidance (2 CFR Part 200). Section 200.425 discusses audit services and states: “A reasonably proportionate share of the costs of audits required by, and performed in accordance with, the Single Audit Act Amendments of 1996 (31 U.S.C. 7501-7507), as implemented by requirements of this part, are allowable.” If you expended funds from multiple federal grant programs in a fiscal year, each program would pay a proportionate share of the cost of the Single Audit.

Yes. Premium pay amounts paid to employees are considered wages. Employers generally must withhold federal income tax as well as social security tax and Medicare tax from employees' wages. (Employers also may have to pay federal unemployment tax on the wages.) Any payment from SLFRF/ARPA that is in the nature of compensation for services, even a one-time payment (such as a hiring "bonus"), is considered wages. More information can be found on the IRS CSLFRF (ARPA) FAQ.

Disclaimer: This resource was created by Municipal Operations Support (MOS) staff of non-legal professionals with expertise of the subject matter. It is only intended to provide information and does NOT constitute legal advice. Readers with legal questions are encouraged to contact an attorney. The use or downloading of this resource does NOT create an attorney-client relationship and will not be treated in a confidential manner. Non-legal questions about this resource can be directed to MOS staff at mos@vlct.org.

For recipients using Fiscal Recovery Funds to provide government services to the extent of reduction in revenue, the description of government services reported to Treasury may be narrative or in another form, and recipients are encouraged to report based on their existing budget processes and to minimize administrative burden. For example, a recipient with $100 in revenue replacement funds available could indicate that $50 were used for personnel costs and $50 were used for pay-go building of sidewalk infrastructure.

In addition to describing the government services provided to the extent of reduction in revenue, all recipients will also be required to indicate that Fiscal Recovery Funds are not used directly to make a deposit in a pension fund. Further, recipients subject to the tax offset provision will be required to provide information necessary to implement this provision. Treasury does not anticipate requiring other types of reporting or recordkeeping on spending in pensions, debt service, or contributions to reserve funds.

(FAQ - Project and Expenditure Report User Guide - Appendix F , 1.4, page 80)

Login.gov is a secure sign in service used by the public to sign in to participating government agencies. Participating agencies, like the U.S. Department of the Treasury, will ask you to create a Login.gov account to securely access your information on their website or application. A Login.gov account is unique to each individual and there is a required authentication method along with a password.

SAM.gov - System for Award Management (SAM.gov) - is an official website of the U.S. Government. A SAM registration is required for any entity to bid on and get paid for federal contracts or to receive federal funds. These include for-profit businesses, nonprofits, government contractors, government subcontractors, state governments, and local municipalities. There is no cost to use SAM.gov. SAM.gov uses Login.gov for a secure sign in to their website.

Treasury's (Compliance and Reporting) Portal - This is a secure website through which Treasury requires all ARPA reporting to be done. To access the Portal, a user must use their unique Login.gov account that is associated with the email address that Treasury has on file for that user (this was provided during the certification process in the summer of 2021).

Registering with SAM.gov is a requirement of your ARPA award (see Terms and Conditions, page 3, item 9.b.ii.), however you do not need to already be registered to access Treasury's portal.

More resources on registering with SAM.gov will be provided on the Treasury website.

Yes, report ALL spending under Expenditure Category 6.1 Provision of Government Services, regardless of the type of project you undertake or spending using your ARPA award.

Source: Treasury 3/21 webinar: https://youtu.be/0NE1ZQXzOWo (minute: 13:55)

Yes. All recipients will have the option to make a one-time decision to elect the “Standard Allowance” of up to $10 million, not to exceed the award allocation during the April 30, 2022 reporting period.

Source: Treasury 3/21 webinar: https://youtu.be/0NE1ZQXzOWo (minute: 30:55)

It is a best practice. Here is sample language for a motion:

"I move that the [town, city, village] of [municipality name] make the one-time irrevocable decision to elect the “Standard Allowance” approach for our ARPA award in the amount of [amount of TOTAL award], to spend on the provision of government services throughout the period of performance of the grant."

The Account Administrator** has the administrative role of maintaining the names and contact information of the designated individuals for SLFRF/ARPA reporting. The Account Administrator is also responsible for working within your organization to determine its designees for the roles of Point of Contact for Reporting and Authorized Representative for Reporting and providing their names and contact information via Treasury’s Portal. Finally, the Account Administrator is responsible for making any changes or updates to the user roles as needed over the award period. We recommend that the Account Administrator identify an individual to serve in his/her place in the event of staff changes.

**Please note, for NEUs, the point of contact (this person is the "Authorized Representative") initially provided to their State for determining eligibility will automatically be designated as an Account Administrator.

The Point of Contact for Reporting is the primary contact for receiving official Treasury notifications about reporting on the SLFRF award, including alerts about upcoming reporting, requirements, and deadlines. The Point of Contact for Reporting is responsible for completing the SLFRF reports however this role does not have the authority to "certify and submit" reports. Only the Authorized Representative for Reporting can "certify and submit" reports.

"Implementation of the Fiscal Recovery Funds also reflects the importance of public input, transparency and accountability." In addition, the IFR establishes certain regular reporting requirements, including requiring local governments to publish information regarding uses of Fiscal Recovery Funds (ARPA) payments in their local jurisdiction. This means your reporting on use of funds will be open for public viewing, perhaps posted on Treasury's website and others, easily found through search engines. "These reporting requirements reflect the need for transparency and accountability." Treasury urges State and local governments "to engage their constituents and communities in developing plans to use these payments, given the scale of funding and potential to catalyze broader economic recovery and rebuilding."

Yes, multiple individuals can be assigned/designated for each role.

Yes, an individual may be assigned/designated for multiple roles.

A record of late reporting could lead to a finding of non-compliance, which could result in development of a corrective action plan, or other consequences.

(Source: Project and Expenditure Report User Guide, Appendix F FAQ, Q 1.17.)

NO! There is no charge for creating or renewing your SAM.gov registration. There are entities that might charge a fee to do this for you but BUYER BEWARE! This is a common phishing/scamming tactic (See this example HERE). To brush up on your cybersecurity knowledge, check out VLCT's Technology and Cybersecurity page.

Yes. The Award Terms and Conditions and the Assurances of Compliance with Civil Rights Requirements both signed and dated by your Authorized Representative together serve as your grant agreement for your ARPA award. It is considered executed even without Treasury signature.

The Assistance Listing Number (ALN), formerly known as the Catalog of Federal Domestic Assistance (CFDA) Number, is a five-digit number assigned in the awarding document for all federal assistance award mechanisms, including federal grants and cooperative agreements.

ARPA's ALN is: 21.027

Eligible uses for APRA funding fall into four broad categories: Public Health/Negative Economic Impacts; Premium Pay; Investments in Water, Sewer & Broadband; and Revenue Loss

Revenue Loss provides recipients with broad discretion to use funds for the provision of government services. This category provides for the most flexibility in use and also has the least burdensome reporting requirements. Even if you are doing a project that would fall under one of the other three categories, you may report it under revenue loss to take advantage of the streamlined reporting (in fact, Treasury has encouraged this!).

How much of our award can we use for Revenue Loss? An entity may use its ARPA award for the provision of government services under the Revenue Loss category to the extent to the entity has lost revenue due to COVID.

So how do we go about determining what the dollar amount of lost revenue due to COVID is? Originally, there was a formula. It was complicated and Treasury received a lot of feedback that it was just too much, and it was changed with the Final Rule. Under the final rule an entity may either (1) still use the formula OR (2) take the Standard Allowance to determine the amount of lost revenue due to COVID.

Treasury’s final rule says that Treasury is presuming all entities experienced lost revenue due to COVID of up to $10 million. As such, any entity may elect the standard allowance and use up to $10 million of their ARPA funds for the provision of government services under the Revenue Loss category without doing the complicated calculation.

All recipients have only ONE CHANCE to elect the standard allowance and that’s as part of the reporting that is due April 30th. Taking the Standard Allowance doesn’t change the amount of your award nor does it constitute an obligation of funds or a project. It just says “We intend to use some or all of our award under Revenue Loss up to the Standard Allowance”. The Project and Expenditure Report asks you to choose whether or not you want to take the standard allowance and how much of your award you are going to use toward lost revenue. The recommendation is to say "YES" we want to take the standard allowance and enter your entire award amount. This eases the overall administrative burden, simplifies the reporting requirements, and allows for the most flexibility in using the funds.

Try following this "SAM.gov Quick Start Guide for Updating Registrations" which can be found HERE.

As you begin to gather feedback on how your local ARPA funds should be spent, you might consider the following questions as you formulate your criteria for uses/requests:

-

Does the use/request follow the intent of the Coronavirus State and Local Fiscal Recovery Funds (aka ARPA)?

-

Fight the pandemic and support families and businesses struggling with its public health and economic impact

-

Maintain vital public services, even amid declines in revenue resulting from the crisis

-

Build a strong, resilient, and equitable recovery by making investments that support long-term growth and opportunity

-

-

Does the use/request comply with the Town Plan?

-

If the Town has a Master Plan or any other plans, studies or reports, is the use/request included in them?

-

If the Town has a Capital Improvement Plan, is the use/request contained in the CIP?

-

Does the use/request set a precedent that will be difficult for the Town to fulfill for others in the future? (ex. stormwater project on private property)

-

Does the use/request create an ongoing expense that will need to be funded with property taxes when ARPA funds have been exhausted? (ex. hiring new Town employees)

-

Does the use/request have broad community benefit or does it benefit just a few?

-

Does the use/request bring long-term value to the community for generations to come?

-

Can the use/request leverage other grant funds? (ex. Town Hall improvements – town could apply for funding through new source from H.518; paving projects – has the Town applied for a paving grant from VTrans?)

-

Can the use/request be redirected to an existing program with the State’s ARPA (or other funds)? (ex. direct assistance to households for housing expenses, refer them to: Housing Resources for Vermonters in Need)

Generally, no. However, after the obligation deadline, if the contract or subaward was entered into prior to December 31, 2024, recipients may replace the contract or subaward under these circumstances:

- The recipient terminates the contract or subaward because of the contractor or subrecipient’s default, the contractor or subrecipient goes out of business, or the recipient determines that the contractor or subrecipient will not be able to perform under the contract or carry out the subaward.

- The recipient and contractor or subrecipient mutually agree to terminate the contract or subaward for convenience.

- The recipient terminates the contract or subaward for convenience if the contract or subaward was not properly awarded, there is clear evidence that the contract or subaward was improper, the recipient documents the determination that it was not properly awarded, and the original contract or subaward was entered into by the recipient in good faith.

See Treasury’s State and Local Fiscal Recovery Funds: Obligation Interim Final Rule (IFR) presentation.

To review a short presentation that discusses three (3) possible approaches you could take to account for ARPA funds in your general ledger, please click HERE.

A subrecipient is an entity that receives a subaward to carry out a project funded by Fiscal Recovery Funds on behalf of a recipient. Individuals or entities that are direct beneficiaries of a project funded by Fiscal Recovery Funds are not considered subrecipients. Households, communities, small businesses, nonprofits, and impacted industries are all potential beneficiaries of projects carried out with SLFRF funds.

The terms and conditions of Federal awards flow down to subawards to subrecipients, requiring subrecipients to comply with all requirements of recipients such as the treatment of eligible uses of funds, procurement, and reporting requirements. Beneficiaries are not subject to the requirements placed on subrecipients in the Uniform Guidance, including audit pursuant to the Single Audit Act and 2 CFR Part 200, Subpart F or subrecipient reporting requirements.

BUT....

Treasury is not collecting subaward data for projects categorized under Expenditure Category Group 6 “Revenue Replacement.” Treasury has determined that there are no subawards under this eligible use category. The definition of subrecipient in the Uniform Guidance provides that a subaward is provided for the purpose of “carrying out” a portion of a federal award. Recipients’ use of revenue loss funds does not give rise to subrecipient relationships given that there is no federal program or purpose to carry out in the case of the revenue loss portion of the award. (Treasury SLFRF FAQs 13.14)

For towns, cities and villages that elected the standard allowance and will spend their funds on the "provision of government services" (Expenditure Category 6.1 Revenue Replacement), then only certain sections of Uniform Guidance (2 CFR Part 200) apply to the use of these funds. Please refer to this 2 CFR Part 200 Table of Contents (modified for revenue loss) that has been highlighted to show these sections. Please note that key sections are not included like Procurement Standards.

For the full text of 2 CFR Part 200, that includes the Table of Contents with the sections that apply to revenue loss highlighted and linked to the applicable language in the body of the +200 page document, click HERE.

(Treasury SLFRF FAQs, 13.15)

Click HERE to view the actual data that was entered for Project & Expenditure Reports during the April 30, 2022 reporting to the U.S. Department of the Treasury. It includes Vermont's NEUs (non-entitlement units of government), metropolitan areas (Burlington and South Burlington), as well as the State of Vermont.

Yes. When you are completing the Subrecipient Annual Report (found HERE), you must include only the ARPA* funds that were expended during your fiscal year for which you are reporting. Here is what you should include for your local ARPA funds:

In Section III - Subrecipient Schedule of Federal Expenditure:

- CFDA Number (Catalog of Federal Domestic Assistance) CFDA numbers have been replaced with ALN (Assistance Listing Number). The ALN for ARPA is 21.027.

- Granting Agency/Department - U.S. Dept. of the Treasury

- Grant Number - Use your assigned "Town ID" number which can be found HERE.

- Expenditures - enter your total ARPA expenditures for the fiscal year on which you are reporting. (DO NOT enter the total amount of your award or the total amount of cash you've received - you report APRA expenditures only.)

* If you expended any ARPA funds as a "subrecipient" of a grant from an entity other than the U.S. Department of the Treasury (ex. a grant from an Agency or Department of the State of Vermont), then you must also report these funds in the Subrecipient Annual Report and do so separately from your local ARPA funds. They will have the same CFDA/ALN Number but the Granting Agency and Grant Number will be different.

If you received any ARPA funds as a "beneficiary," then you do not need to include these funds in this report.

If you are unsure whether you are "subrecipient" or a "beneficiary," please read this FAQ: What is the difference between a "beneficiary" and a "subrecipient"? and if you are still unsure, then reach out to the Agency, Department or entity that awarded the funds to your town/city/village.

The State and Local Fiscal Recovery Funds (SLFRF, aka ARPA) program provides governments across the country with the resources needed to:

- Fight the pandemic and support families and businesses struggling with its public health and economic impacts

- Maintain vital public services, even amid declines in revenue resulting from the crisis

- Build a strong, resilient, and equitable recovery by making investments that support long-term growth and opportunity

ARPA includes four broad criteria outlining eligible uses:

-

To respond to the public health emergency or its negative economic impacts, including assistance to households, small businesses, and nonprofits, or aid to impacted industries such as tourism, travel, and hospitality;

-

To respond to workers performing essential work during the COVID-19 public health emergency by providing premium pay to eligible workers;

-

For the provision of government services to the extent of the reduction in revenue due to the COVID–19 public health emergency relative to revenues collected in the most recent full fiscal year prior to the emergency*; and

-

To make necessary investments in water, sewer, or broadband infrastructure.

On January 6, 2022, the U.S. Department of the Treasury issued the Final Rule that further explains eligible and ineligible uses. Recipients may also find the Overview of the Final Rule helpful,. It provides a summary of major provisions of the Final Rule for informational purposes.

* If your town, city, or village elected to the "standard allowance," then it may use the amount of the reduction of revenue (in most cases the full amount of award) on the "provision of government services."

Yes. VLCT created an annotated version of the ARPA Terms & Conditions document. The annotated version can be found HERE.

Yes. It can be found HERE.

No, ARPA money does not need to be in a separate cash (bank) account. Best practice is to create a separate fund in the general ledger to more easily account for and report on these funds.

Also, any interest earned on this money may be kept by the municipality.

Yes, provided that the project is itself an eligible use of funds and that the award recipients can track the use of funds in line with the reporting and compliance requirements of the Coronavirus Local Fiscal Recovery Funds/ARPA. In general, when pooling funds for regional projects, recipients may expend funds directly on the project or transfer* funds to another government that is undertaking the project on behalf of multiple recipients. To the extent recipients undertake regional projects via transfer to another government, recipients would need to comply with the rules on transfers specified in the Interim Final Rule, Section V. A recipient may transfer funds to a government outside its boundaries (e.g., county transfers to a neighboring county), provided that the recipient can document that its jurisdiction receives a benefit proportionate to the amount contributed.

Visit the Code of Federal Regulations website here: https://www.ecfr.gov/current/title-2/subtitle-A/chapter-II/part-200

ARPA funds must be obligated by December 31, 2024. Any funds not obligated by this date must be returned to Treasury.

ARPA funds must be expended by December 31, 2026. Any funds not expended by this date must be returned to Treasury.

Just transferring your ARPA funds into your general fund does not meet the definition for obligated.

“Allocating," "appropriating,” “designating,” “setting aside,” “reserving,” etc. your ARPA funds does not meet the definition for obligated.

In November 2023, the U.S. Treasury issued the Obligation Interim Final Rule (IFR) to address recipients’ questions and comments regarding the definition of obligation. The Obligation IFR revises the definition of “obligation” in Treasury’s implementing regulations for the SLFRF (ARPA) program and provides related guidance to give additional flexibility and clarity to recipients to support their use of SLFRF funds. Treasury created a two-page “Quick Reference Guide” that informally summarizes the 17-page Obligation IFR.

From Treasury SLFRF FAQs 13.17:

"As stated in the final rule, obligation means “an order placed for property and services and entering into contracts, subawards, and similar transactions that require payment.” See 31 CFR 35.3.

(Also see Treasury’s State and Local Fiscal Recovery Funds: Obligation Interim Final Rule (IFR) presentation for more details, examples and explanation.)

Recipients can use ARPA funds on government services up to the revenue loss amount (in most cases in Vermont, the entire ARPA award), whether that be the standard allowance amount or the amount calculated using the above approach. Government services generally include any service traditionally provided by a government, unless Treasury has stated otherwise*. Here are some common examples, although this list is not exhaustive:

✓ Construction of schools and hospitals

✓ Road building and maintenance, and other infrastructure

✓ Health services

✓ General government administration, staff, and administrative facilities

✓ Environmental remediation

✓ Provision of police, fire, and other public safety services (including purchase of fire trucks and police vehicles)

* Restrictions:

✓ No deposits into pension funds

✓ No debt service or replenishing financial reserves

✓ No satisfaction of settlements and judgments

✓ No project that conflicts with or contravenes the purpose of the American Rescue Plan Act statute (e.g., uses of funds that undermine COVID-19 mitigation practices in line with CDC guidance and recommendations) and may not be used in violation of the Award Terms and Conditions or conflict of interest requirements under the Uniform Guidance. Other applicable laws and regulations, outside of SLFRF program requirements, may also apply (e.g., laws around procurement, contracting, conflicts-of-interest, environmental standards, or civil rights).

From the award Terms and Conditions, item 2. "The period of performance for this award begins on the date hereof and ends on December 31, 2026." The "date hereof" is the date your Authorized Representative signed the cover page of the Terms and Conditions document

No. Treasury presumes that revenue has been lost due to the public health emergency and recipients are permitted to use that standard allowance approach (not to exceed the award amount) to fund “government services.”

Treasury's methodology for determining the $10 million standard allowance is discussed in the final rule on page 240; presumption is on page 249

Most of the provisions of the Uniform Guidance (2 CFR Part 200) apply to this program, including the Cost Principles and Single Audit Act requirements. Recipients should refer to the Assistance Listing for detail on the specific provisions of the Uniform Guidance that do not apply to this program. The Assistance Listing will be available on beta.SAM.gov.

Treasury FAQ 9.3

An Authorized Representative is an individual with legal authority to bind the government entity (e.g., the Chief Executive Officer of the government entity). An Authorized Representative must sign the Acceptance of Award terms for it to be valid.

Treasury FAQ 11.7

When you completed your certification to receive ARPA funds through the State of Vermont's online certification portal, you would have entered the name and contact information for your Authorized Representative as a required field.

NEUs are considered prime recipients of Treasury and States are not responsible for monitoring NEUs for compliance with use of funds.

Disclaimer: This resource was created by Municipal Operations Support (MOS) staff of non-legal professionals with expertise of the subject matter. It is only intended to provide information and does NOT constitute legal advice. Readers with legal questions are encouraged to contact an attorney. The use or downloading of this resource does NOT create an attorney-client relationship and will not be treated in a confidential manner. Non-legal questions about this resource can be directed to MOS staff at mos@vlct.org.