Vermont municipalities continue to step up their efforts to achieve climate resilience through clean vehicle purchases, clean energy and infrastructure development, and energy efficient building improvements. Unique provisions in the federal Inflation Reduction Act (IRA) of 2022 opened federal tax credits and incentives to municipalities and other tax-exempt entities. These incentives can lower the total cost of projects substantially when their requirements are incorporated into the project’s development.

How can non-tax paying entities use the Inflation Reduction Act’s tax incentives?

In the Inflation Reduction Act (IRA) of 2022, Congress authorized entities that don’t pay federal taxes, such as municipalities and municipal utilities, to use certain tax incentives through two mechanisms:

- Direct Pay (Refundability) allows a non-tax paying entity to receive a cash payment (refund) from the IRS for the tax credit. The municipal direct-pay options are effective beginning tax year 2023. When available, notification about the forms and instructions for monetizing direct pay tax credits will be posted to the IRS’ IRA webpage.

- Transfer of Credit (Transferability) allows non-tax paying entities to sell all or a portion of a tax credit to an unrelated eligible taxpayer.

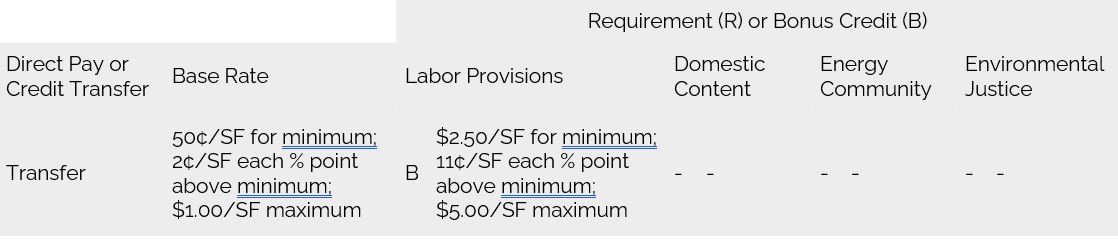

Credits available to municipalities are Direct Pay except for the energy efficient commercial building tax deduction.

What tax credits and tax deductions are available?

Relevant tax credits for Vermont municipalities are described below. Production Tax Credits provide a subsidy over time, based on kilowatt hour of energy produced and sold. Investment Tax Credits provide a subsidy to stimulate investment in specific activities. The credits have two tiers: a “base rate” and one or more “bonus rates”. To qualify for a bonus, certain requirements must be met. Most bonuses are stackable, meaning they are additive to the base rate. In some cases, meeting all bonus requirements provides a tax credit of 50-60% of the project cost. Guidance for these tax new provisions is pending from the US Treasury and Internal Revenue Service.

Production Tax Credits

Renewable Energy Generation Tax Credit (§ 45)

- Placed in service after 12/31/22 or construction begins before 01/01/25

- Labor standards not required for projects <1 MW

- Increases hydropower & municipal solid waste to full value (was half value)

- Power must be produced and sold

- Using tax-exempt bonds reduces credit value (IRC § 45(b)(3))

Clean Electricity Production Tax Credit (§ 45Y)

- ≤Zero emissions required

- Placed in service after 12/31/24; 10-year term

- Credit phase out when emission target achieved or by 2032

- Credit phase out if domestic content requirements not met for ≥1 MW

- Credit value 100% year 1, 75% year 2, 50% year 3, then 0%

- Using tax-exempt bonds reduces credit value (IRC § 45(b)(3))

Investment Tax Credits & Deduction

Vehicle Refueling Tax Credit (§ 30C)

- Placed in service between 2023-2032

- Capped at $100,000 per single item

- Low-income (IRC § 40D9(e)) or non-urban census tracts only

- Property must be subject to depreciation

Commercial Clean Vehicles Tax Credit (§45W)

- Base rate is 15-30% depending on power source, or the incremental cost of such vehicle, whichever is less

- Placed in service between 2023-2032

- IRS designates eligible vehicles and annual tax credit rate. For 2023, rates are:

- $7,000* compact car Plug-in Hybrid Electric Vehicle

- $7,500* other vehicles up to 14,000 pounds with ≥7 kWh battery

- $40,000* mobile machinery (all other vehicles plus those under 26 USC § 4053(8); ex. commercial lawnmower, fork lift, off highway vehicle)

- Depreciable property requirement doesn’t apply

Energy Tax Credit (§ 48)

- Base rate is 30% if <1 MW OR project ≥1 MW and began construction ≤ 01/29/23 OR prevailing wage met for construction + 5 years & apprenticeship met during construction

- Construction must begin prior to 01/01/25; geothermal prior to 2035

- Same rates for standalone energy storage; capacity requirements and construction start applies

- Storage connected to generation facility can be included in the facility’s tax credit or can use the standalone provision

- Projects ≥1 MW have separate domestic content requirements based on when construction begins (will need IRS guidance)

- Interconnection capital costs eligible for projects ≤5 MW

- Using tax-exempt bonds reduces credit value (IRC § 45(b)(3))

Clean Electricity Investment Tax Credit (§ 48E)

- ≤Zero emissions required, except for storage technology and thermal storage properties

- Base rate is 30% if <1 MW OR project ≥1 MW and began construction ≤ 01/29/23 OR prevailing wage met for construction + 5 years & apprenticeship met during construction

- Placed in service after 2024

- Solar & wind generation of <5 MW only have Environmental Justice (EJ) bonuses:

- 10% bonus if facility connected with a low-income community

- 20% bonus if facility connected with low-income residential building or low-income economic benefit project

- Credits allocated by Secretary of Treasury to qualify; calendar year capacity limit applies

- Standalone storage not eligible for EJ bonus

- Credit value when taken is 100% year 1, 75% year 2, 50% year 3, then 0%

Energy Efficient Building Tax Deduction (§ 179D)

- Minimum 25% increase in efficiency required

- Placed in service beginning 01/01/23; Expires 12/31/31

- Government buildings qualify

- Applies to new construction and retrofits

- Allocation letter required for credit transfer to project designer

- Energy efficiency standards per IRS Bulletin 2023-1 required

- Requires inspection, verification, and certification by a licensed engineer or contractor

- US DOE qualified software required for efficiency calculations

*Value adjusted annually and/or value will be modified due to a formula change in IRA. See IRS’ IRA website.

What are the bonuses that apply to base rates?

Bonus rate requirements vary by tax credit. Bonus rate criteria include:

- Prevailing Wage: Federal prevailing wages, informally known as Davis-Bacon wages, must be paid to laborers and mechanics participating in construction, alternation, and repair activities. Prevailing wage is mandatory to earn certain base credits. See VLCT’s Guide to Obtaining Federal Davis-Bacon Wage Determinations.

- Apprenticeship: A percentage of total labor hours must be provided by qualified apprentices. The percentage is based when construction begins: 10% through December 31, 2022; 12.5% during calendar year 2023; and 15% beginning January 1, 2024. Apprenticeships are mandatory for some credits. The Vermont Department of Labor maintains a list of Registered Apprenticeship Sponsors. A contractor can request a waiver. The bonus credit is awarded if the contractor made a Good Faith Effort (§ 45(b)(8)) and there are no available qualified apprentices.

- Domestic Content: Projects must be constructed using domestically sourced steel and iron, as well as manufactured products, and construction materials must be manufactured in the United States. This Fact Sheet and FAQ from the Federal Emergency Management Agency (FEMA) describes requirements. IRA phases in domestic content requirements for manufactured products based on when construction begins: 40% through December 31, 2024; 45% during calendar year 2025; 50% during calendar year 2026; and 55% beginning January 1, 2027. Federal funds recipients are required to certify, or provide equivalent documentation, regarding proof of compliance. Approved waivers are listed on agency websites and on MadeinAmerica.gov.

- Energy Communities: Project must be located on a brownfield site or in a former fossil fuel community. Vermont’s qualification is expected to be for brownfield sites. A few northern census tracts may qualify based on natural gas. The Vermont Agency of Natural Resources maintains a searchable Brownfield Site List as part of its Vermont Environmental Research Tool. The US Treasury will develop guidance for this definition.

- Environmental Justice: Project must be located in a low-income community (IRC § 45D(e)) or non-urban census tract, benefit a low-income residential building (IRC § 48E(h)(2)(B)), or provide a low-income economic benefit (IRC § 48E(h)(2)(C)).

Which projects benefit more from Production versus Investment Tax Credits?

Projects using Production Tax Credits must sell the power produced to an unrelated party. In general, large-scale projects will receive more value from the Production Tax Credit. Based on current technology, the Investment Tax Credit generally works better for smaller scale projects, larger scale photovoltaic projects in less sunny locations, projects incurring high installation costs, or projects qualifying for bonus credits. (Adapted from US Department of Energy, Federal Solar Tax Credits for Businesses).

What should municipalities understand now?

The details of implementing the new law are under development. For now, municipalities should understand that:

- monetizing the credits and deductions can lower purchase and development costs.

- project size, final IRS requirements, and other factors will determine whether tax incentives are beneficial.

- per IRS guidance, using these tax credits may reduce the depreciable value of an asset.

- meeting labor provisions is required to earn the base rate for some credits. For other credits, they are an opportunity to achieve significant bonuses (6% credit è 30% credit). Meeting all bonus requirements can increase a total credit to 50-60% for some incentives.

- using renewable energy generation tax credits may outweigh the savings from using tax-exempt bonds, even though they lower the value of the credits (26 US Code § 45(b)(3)).

- tax credits can be included in a project’s list of funding sources alongside federal or state grants. Direct-pay tax credits may be eligible as a local match contribution to a grant. Tax credits under different sections of Federal code cannot be used together (no double tax benefit, a.k.a. “double-dipping”).

- some tax credits are time sensitive. For tax credits §§ 30C, 45, 45Y, 48, 48E, and 179D, the IRS defined Beginning Construction to mean either beginning physical work of a significant nature or paying or incurring 5% of more of the total costs of the facility. Project progress must be made through continuous construction or continuous effort (no stopping work after Beginning).

- Power production, alternative fuel vehicle, and energy efficient building projects must be related to the municipality’s tax-exempt purpose. If a project involves income generated from private parties (ex. leased public building or EV charging power purchase agreement), consult a tax professional. All or a portion of the project may be deemed ineligible for tax incentives.

For information about how to claim tax incentives, visit our resource on Claiming Tax Incentives for Your Clean Energy Project.

Disclaimer: This summary provides preliminary information about tax credits and deductions available to municipalities through the Inflation Reduction Act of 2022. Links to other sites offered in this document are provided to assist municipalities. The inclusion of a link does not imply endorsement or approval of the linked site. The content of this document does not constitute legal or other professional advice. Municipalities are advised to consult tax, legal and other professionals regarding use of these credits.

Print linked PDF file for accessible version of document that includes the summary tables of tax credits.