Model Fraud Prevention Policy + Guidance

Publication Date

03/31/2026

The Vermont League of Cities and Towns (VLCT) has launched CHIP – Invest in Vermont (CHIP IN VT), a three-year initiative designed to help municipalities use Vermont’s new Community and Housing Infrastructure Program (CHIP).

CHIP is an innovative financing program that has potential to help communities fund the infrastructure improvements they need to support new housing — without raising broad based property taxes. While CHIP creates new opportunities, implementing it will require more staff hours and technical expertise than many of Vermont’s towns, cities, and villages have. VLCT has designed CHIP IN VT to help close this capacity gap by providing local governments with practical training, tools, and ongoing technical assistance.

“Communities across Vermont are ready to address housing needs, but infrastructure costs and limited local capacity often stand in the way,” said Ted Brady, Executive Director of VLCT. “CHIP IN VT will give local leaders the knowledge, resources, and confidence they need to make good use of the funding opportunities that the legislature made possible with CHIP.”

CHIP IN VT offers learning pathways tailored to meet the specific situations of interested municipalities. Local officials will have access to educational sessions, cohort-based learning opportunities, and technical assistance in addition to a growing library of tools, templates, and guidance. Over time, participants will build the skills and relationships needed to evaluate project feasibility, prepare strong CHIP applications, and manage the long-term responsibilities that CHIP requires.

“Local officials are juggling many priorities, and complex financing programs can feel overwhelming,” said Katie Buckley, Director of Municipal Operations Support at VLCT. “CHIP IN VT is designed to make CHIP easier for communities of all sizes to use – so they can take advantage of this historic opportunity to grow their housing supply.”

By strengthening municipal workforce capacity, CHIP IN VT aims to accelerate infrastructure investments that not only make housing development possible but also support economic growth and help communities plan for long-term sustainability.

Learn more about CHIP IN VT at vlct.org/CHIP. Learn more about Vermont’s Community and Housing Infrastructure Program (CHIP) at accd.vermont.gov/economic-development/vepc/chip.

CHIP IN VT is an effort funded by a $500,000 (70%) grant from the Northern Borders Regional Commission, a $200,000 (28%) grant from the State of Vermont Agency of Administration and a $10,000 (2%) contribution from the Vermont League of Cities and Towns.

Without this funding VLCT would not be able to offer this assistance to its membership which consists of towns, cities, villages, counties, housing authorities, solid waste districts, fire districts, regional planning agencies, communications union districts, and other political subdivisions of the State of Vermont.

The capital assets of a town and their condition are critical to the quality of services that a municipality can provide. Capital asset expenditures can be more controversial than other expenditures because they typically involve large sums of money, often raised through debt financing, and not every citizen will agree as to the necessity of each project that is undertaken. By using a well thought out capital improvement program, the town can plan for replacement of assets, potential capital reserve funding, operating budget expenditures, and debt service expenditures.

Vermont law provides for adoption of a capital budget and plan at 24 V.S.A. § 4430 and encourages that the capital improvement plan conforms to the municipal plan.

Capital improvement policies need to be general and flexible to accommodate a community’s political will while still providing enough guidance to enable sound financial choices. Therefore, the policy will generally consist of guidelines designed to stimulate an informed debate to encourage the most enlightened choices, rather than trying to force efficient or effective decisions by way of a rigid menu of policy choices. Determining the criteria for selecting projects in advance will take the emotion out of the selection process.

Consider the following when developing a capital improvement policy:

Capital Improvement Program. The basis of any capital improvement plan is the capital improvement program (CIP), a five-year projection of the town’s capital needs and its available financial resources. The purpose of the CIP is to help build consensus on what are the most important projects, thus ensuring these projects are undertaken first. The policy needs to include the criteria that will be used to prioritize the projects that are included in the plan.

Project Financing. There are numerous alternatives for financing capital projects, from pay-as-you-go financing or accumulation of reserve funds to leases and other debt instruments. The policy should include a discussion of the town’s preferred financing methods.

For more information on capital planning, please see the Vermont Land Use Planning Implementation Manual, published by the Vermont Land Use Education and Training Collaborative. The Implementation Manual is available at www.vpic.info.

Please note that this model policy has been developed for illustrative purposes only. VLCT makes no express or implied endorsement or recommendation of any financial policy, nor does it make any express or implied guarantee of legal enforceability or legal compliance, nor does VLCT represent that any particular policy is appropriate for any particular municipality. Your legal counsel should review any proposed financial policy before adopting it.

As always, please contact the Municipal Assistance Center if you have questions at info@vlct.org or 800-649-7915.

Capital planning helps towns prepare for the future. It’s a way to make important decisions about big projects - like fixing roads, building a new highway garage, or replacing water pipes - before problems happen. Taxpayers often ask, “Why plan so far ahead?” The answer is simple: planning saves money, reduces costly surprises, and helps the town prepare for emergencies – from sudden repairs to natural disasters. A capital plan makes sure tax dollars are used wisely, and the town doesn’t promise more than it can afford.

A capital plan is a long-term guide for big investments like buildings, roads, equipment, and land. It helps towns know what they own, what needs fixing, and what they’ll need in the future. Capital projects take time and money. Planning helps make sure they’re done right.

Capital planning is like using a map - it helps the town avoid wrong turns, save money, and reach its goals. It’s not just about buildings and roads; it’s about making sure the community stays strong, safe, and equipped for tomorrow. Planning doesn’t mean spending more money. It means spending money wisely. Without a plan, the town risks wasting money, missing out on grants, and falling behind on basic services. With a good plan, the town stays resilient, stable, and ready for whatever comes next.

VLCT has a robust list of resources to help with capital planning. Whether your municipality is just thinking about it or is ready to take it to the next level, we are here to help. And as always, if you need a human to help you navigate, don't hesitate to ask us! Email the Municipal Operations Support Team: mos@vlct.org.

It’s the day after the Super Bowl and we’re hoping our 2026 legislative season shapes up a little better than the Patriots’ game did. The VLCT advocacy team spent last week mired in discussions over major land use issues. We think it’s fair to say that we are putting up a strong offense for Act 181 reforms and a number of exciting new housing bills. We were surprised to be put on the defense with new proposals in the agriculture bills that would roll back municipal authority over non-farm animals. Meanwhile, the governor this week went public with his playbook for Act 181 reforms.

In this Weekly Legislative Report, we outline the House and Senate proposals to address municipal authority over agricultural activity, provide an update on proposed Act 181 reforms and debate, and are pleased to announce the opening of the CHIP application portal and upcoming VLCT CHIP programs.

For a long time, the conventional wisdom was that farms subject to the state’s Required Agricultural Practices (RAPs) were afforded a broad exemption from municipal zoning regulation. However, in May of this year the Vermont Supreme Court issued a decision – explained by both VTDigger and VLCT – that appears to dramatically change the landscape of municipal zoning in terms of the scope of the agricultural exemption for certain activities and structures.

Since the start of the session, each chamber's agriculture committee has heard testimony on the question of municipal authority. Last week each committee released new bill language that attempts to provide clarity to the law.

The VLCT Advocacy team testified earlier this session and has proposed new municipal authority over agriculture practices in Tier 1 areas only, while supporting a total exemption from municipal regulation for farms outside of Tier 1 – more than 98% of the state. VLCT also supports a new provision to create a right to grow food regardless of farm designation status (more on that later).

The Senate’s bill, S.232, largely follows the request made by the Agency for Agriculture, Food & Markets (AAFM) to exempt all designated farms from municipal regulation except for farms operating on less than one acre. It also makes changes to the RAPs so that for an operation to be determined to be farm (thus exempted from municipal zoning) it would have to make more than $5,000 in sales per year (up from $2,000). For farms raising livestock on one to four (1-4) acres of contiguous land, the Secretary of the agency would have discretion to determine, in consultation with the municipality, whether the livestock are causing significant adverse water quality impacts and if the RAPs should apply. While this proposal helps close a current regulatory gap pertaining to small-scale farms with livestock, it does not address VLCT’s concerns about managing the effects of future farming inside of complex, dense, multi-use zoning districts with Act 250 exemption in Tier 1A and 1B.

The House bill more closely aligns with VLCT’s goals. It would exempt all farms subject to the RAPs from municipal zoning but would allow municipalities to regulate new construction of farm structures in Tier 1A areas only. Farm structure is defined as “a building, enclosure, or fence for housing livestock, raising horticultural or agronomic plants, or carrying out other practices associated with accepted agricultural or farming practices, including a silo, but excludes a dwelling for human habitation.” The House bill does not make any changes to the RAPs for farm acreage or sales income thresholds – a key issue for the farm group coalition, which has opposed opening the RAPs.

While each committee has taken a different approach to drawing lines around municipal authorities over farms and farm structures, they share a common element that VLCT strongly opposes. Both bills would dramatically roll back municipal authority over the care and keeping of livestock on property that is not a designated farm.

For as long as people have lived in Vermont, they have lived with animals. And for just about as long as government has been organized in Vermont, cities and towns have maintained broad authority over the regulation of animals living in homes and on homesteads.

Municipal animal ordinances, including those related to livestock, ensure that animals and people can live together in Vermont in a safe and orderly way. Municipal regulations also create a critical opportunity for law enforcement to step in and facilitate forfeiture when animals are being kept in unclean or inadequate shelters, or in instances of hoarding.

The long-existing municipal authority over non-farm animals is why cities, towns, and villages can enforce leash laws (aka at-large dog ordinances), as well as require that animal waste (like horse poop) be composted away from homes, the animal’s shelter, and potable water sources. While these seem like commonsense components of animal ownership, it’s up to local government to keep the rules and to enforce them.

While every municipality in Vermont allows backyard chickens, many local bylaws or ordinances require that coops be secured from predators (including at-large dogs) or that the yard be fenced, or they limit the total number of chickens and/or other types of laying fowl allowed. While committee discussions have revealed that not everyone is a fan of roosters, the truth is many municipalities allow for the keeping of roosters and other types of noisy but useful birds such as toms, guinea hens, or geese – under the appropriate circumstances. Burlington does have a bird ban on the books... for emus.

The proposed prohibition on municipal regulation for off-farm livestock came about when VLCT agreed with AAFM and the farm group coalition (which includes organizations like NOFA, the Farm Bureau, and Rural Vermont) that all Vermonters should have a right to grow food. VLCT supports a provision that would prevent municipal bylaws from prohibiting the growing of food including plants, fruit trees, and sugar trees. This would allow homeowners and renters, as well as businesses and non-profits, to host community gardens or to grow fruits and vegetables for themselves and their community – as long as the gardens and necessary structures (like greenhouses and sugar shacks) meet basic requirements such as setbacks.

We, however, strongly oppose an additional provision that says a municipal bylaw could not regulate the raising, feeding, or managing of livestock “excluding roosters” for use by the owner’s household or nonpaying guests “provided the land base is sufficient for appropriate nutrient and waste management as determined by the Secretary of Agriculture, Food and Markets and the raising, feeding, or managing of livestock is otherwise in compliance with the Required Agricultural Practices Rule.”

This would inhibit municipal regulation over animals and animal shelters on homesteads.

VLCT testified against this provision to the Senate Committee on Agriculture on Tuesday and to the House Committee on Agriculture on Friday, and will keep working lawmakers to help them understand that any rollback of this key municipal authority would cause a stampede of new neighborhood disputes as well as put some pets and livestock at greater risk of unchecked abuse or neglect.

At Governor Scott’s regular press conference last week, he focused on challenges and opportunities related to Vermont’s housing shortage.

The governor again called for bipartisan action during this legislative session to remove regulatory barriers to new housing, including a full repeal of the “Road Rule” which is set to take effect this July, per Act 181 of 2024. Housing Commissioner Alex Farrell said that while future Act 250-exempted areas in Tier 1 are projected to be about 2% of Vermont’s total land area, the Road Rule and Tier 3 areas together would impede new housing development over more than 80% of the state.

Governor Scott referred to the 2024 state election, saying that many or most lawmakers now serving had campaigned on support for more housing and “Now is the time to step up and prove it.”

Administration officials discussed a number of the governor’s proposed reforms to Act 181 including: to eliminate the requirement for municipalities to enforce existing Act 250 permits in Tier 1A areas; to require towns to opt out of Tier 1B rather than opt in to it ; and to require municipal plans to adopt local housing targets or to document barriers to achieving local housing goals such as a lack of developable area, significant flood hazard zone, a lack of water or sewer capacity, or other impediments to growth.

Secretary of the Agency of Commerce and Community Development Lindsay Kurrle said that since 2021 Vermont has invested about $700 million of state and federal funds to housing initiatives which created around 2,000 net new units of housing. The state has adopted housing targets which call for more than 30,000 new units by 2030.

Two critical bills related to Act 181 implementation have been introduced in the House and committed to the House Committee on Environment. H.602 carries the governor’s slate of land use priorities. H.730 is sponsored by the tri-partisan co-chairs of the Rural Caucus – Representative Lisa Hango, Representative Monique Priestley, and Representative Laura Sibilia. House Environment Chair Amy Sheldon has not yet committed to taking up the bills.

Chair Sheldon has recently been absent from the committee, creating an unusual circumstance leveraged by House Republicans who attempted to force a vote by the full chamber on a separate land use bill last week. The procedural vote failed along party lines 86 to 48. Barre Republican Gina Galfetti called the question, saying “A certain committee is unwilling to move bills on housing, energy and other things. It’s time for this body to move legislation that all Vermonters sent us here to move.”

In the Senate, Act 181 implementation will be the subject of a joint hearing of the Committee on Natural Resources and Energy and the Committee on Economic Development, Housing and General Affairs.

At the regular Rural Caucus meeting last Wednesday, Natural Resources Chair Senator Anne Watson pledged to take up the question of Act 181 reforms, saying she intends to spend the majority of the committee’s time between now and crossover on land use issues. Senator Kesha Ram Hinsdale shared her concerns about the trajectory of the mapping process, saying that Act 181 was intended to “be a plan for growth, not to design for decay.”

Last week, Governor Phil Scott and officials from the Agency of Commerce and Community Development (ACCD) announced that the application portal for the Community and Housing Infrastructure Program (CHIP) is officially open.

Secretary of Commerce and Community Development Lindsay Kurrle said: “CHIP opens the door for rural and smaller communities across Vermont to access a financing tool that has historically been out of reach and will help create the housing employers need to recruit and retain workers.”

CHIP will be the most significant investment in municipal infrastructure in state history, allowing up to $2 billion of state investment over the next 10 years to be spent by Vermont communities on infrastructure that will serve a public good and support the development of new housing. The $2 billion “cap” does not include municipal side tax increment investment, which could approach an additional $1 billion, or other public monies that could be combined or “stacked” with CHIP financing, such as SRF, Downtown Tax Credits, federal grants, or the new Housing Infrastructure revolving loan fund offered by the Vermont Bond Bank (also created by Act 69 of 2025).

Over the next decade, CHIP will create thousands and thousands of new homes. Joint Fiscal Office modeling projects that, if the program is fully subscribed, it could add at least $600 million to the state’s flailing education fund by 2059 without raising taxes or rates on existing homeowners and renters.

The state’s new CHIP webpage provides resources:

VLCT will be hosting a free webinar “Introducing CHIP – Vermont's $2B Housing and Infrastructure Program” next week on Thursday, February 19 from 10 AM to 12 PM. Presenters include VLCT staff from the Municipal Operations Support Team and VEPC Executive Director Jessica Hartleben.

This session will provide a clear overview of CHIP, including:

VLCT has received a grant from the Northern Borders Regional Commission that will support a new three-year technical assistance training program called CHIP IN VT. Jessica has shared with us that three Vermont municipalities are already in the CHIP application process. Attend VLCT’s upcoming webinar and leverage our technical assistance tools to help your town or city become CHIP-ready!

Here are some recently released reports and news stories related to top issues for local government.

With work in the State House underway, the most important key to our success is your input and participation in VLCT’s advocacy work. Don’t forget to register to attend our Advocacy Chats to learn what mid-session progress has been made on the issues that matter most to local government. Also, hear what your municipal colleagues from around the state have to say about the hot topics and share your concerns for the legislature. You can register here to join us on Monday, February 23 at 1 PM.

VLCT's "Selectboard Grant Pre-Application Form" template can be used by Selectboards to ensure that all grant activity involving the Town is intentional, coordinated, and aligned with municipal priorities. By requiring review and approval before an application is submitted, the selectboard retains oversight of how the Town’s name, assets, staff time/capacity, and financial resources may be committed—often long before a grant is awarded.

VLCT has updated its FEMA Public Assistance FAQ webpage to address two issues related to FEMA’s Small Project procedure: changes to project scope and what happens when a Small Project costs less than expected.

Several municipalities have asked whether they can adjust how a FEMA‑funded project is carried out. The answer is simple: contact the State of Vermont before making any changes.

FEMA must approve any modification to the scope of work written in the project worksheet. This includes changes to materials, methods, or hazard mitigation components. Scope changes must be approved in writing through a revised project worksheet. Completing work differently than approved – even if the project still functions as intended – can put funding at risk.

During final inspection, if the completed work does not match FEMA’s approved scope, the state may:

Misconduct is treated seriously under federal law. Improper use of FEMA funds can lead to repayment, state or federal debarment, civil penalties, or criminal charges. Early communication with the state is the best way to avoid these outcomes. Best practice is to put your scope change question in writing and get any scope change approval response in writing too.

Under FEMA’s Small Project rules, municipalities may keep excess funds only if:

For highway projects, VTrans will confirm that the work matches the approved scope. Once the state closes the project, any remaining funds may stay with the municipality, but they may still be subject to adjustment later.

To avoid complications, municipalities are encouraged to wait until they receive the final closeout letter for the entire disaster grant before treating any funds as surplus.

These updates are designed to help communities avoid common pitfalls and stay compliant with FEMA requirements. Municipalities are encouraged to review the full FAQ page and reach out to their State Public Assistance Coordinator with questions as projects move forward.

Selectboard onboarding and development are essential to effective local governance. New members step into complex legal, financial, and policy responsibilities that affect every resident, and a clear onboarding process helps them contribute confidently and avoid missteps. Ongoing development keeps the full board aligned, informed, and working as a team. Getting started can be simple: create a concise orientation packet (charter, bylaws, key policies, budget overview), schedule a brief onboarding meeting with the chair and town manager or administrator (if applicable), and plan at least one annual retreat or training session. These small steps build shared understanding, improve decision-making, and strengthen trust in local government.

The following templates, tools and resources can help new selectboard members better understand the "how to" aspects of the role they are taking on. They can also help existing boards adopt new processes and practices to improve upon how they are currently carrying out their work. At VLCT all dogs - new and old - can learn new tricks.

*Plato

Testimony to the Senate Committee on Government Operations

Regarding Municipal Unassigned Fund Balance Authority

Josh Hanford, Director of Intergovernmental Relations, VLCT

Samantha Sheehan, Municipal Policy and Advocacy Specialist, VLCT

January 8, 2026

The Flood Bill included several actions targeting support to municipalities to enable the preparation, emergency response, and recovery from flood disasters and other all hazard events and changed the LOT withholding formula from 70/30 to 75/25.

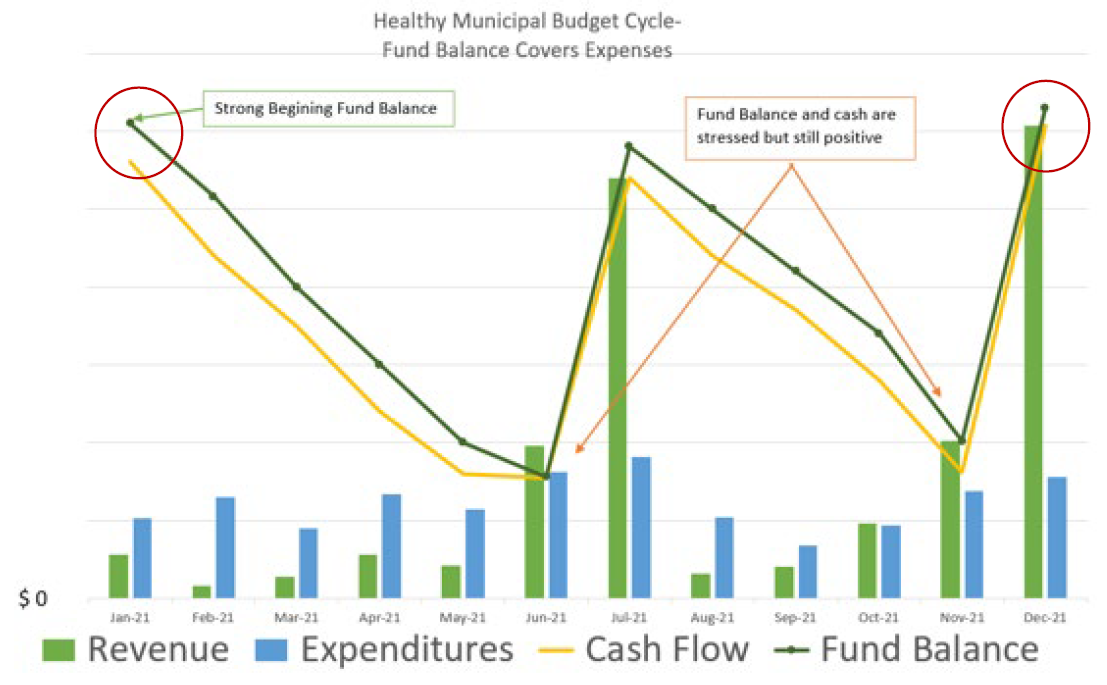

Think of these more like an adjective…..less like a budget line or bank account.

Fund balance is a key component of municipal financial management, providing resources that help manage risk, stabilize tax rates, and maintain services.

An Unassigned Fund Balance is not excess money accumulated unnecessarily to reduce or “buy down” taxes.

Adequate fund balance allows the municipality to continue public services during periods of constrained cash flow (before propertytax payments) without relying on short term debts such as a Tax Anticipation Note (TAN).

Image from New Hampshire Municipal Alliance

Act 57 grants the municipal legislative body control over these funds without additional voter approval.

Selectboards are encouraged to adopt a formal fund balance policy that:

Fund balance levels should be reviewed regularly and adjusted based on:

Municipal cash flow is uneven, with expenses incurred year-round and revenues collected at specific times. In Vermont, municipal revenue authorities are very limited, and most municipalities rely primarily on municipal property taxes.

The Unassigned Fund Balance authority created by Act 57 became effective July 1, 2025.

“Fund Balance Guidelines for the General Fund” Government Finance Officers by GFOA

Taking the Mystery Out of Fund Balance, New Hampshire Municipal Association

Moody’s Rating Methodology, US Local Government General Obligation Debt

Example fund balance policy, City of Burlington

Two exciting revisions regarding municipal finance (in Act 57) took effect on July 1, 2025, thanks to our Advocacy Team’s efforts. They helped secure new provisions of law that allow legislative bodies (selectboards, city councils, etc.) to carry forward unassigned fund balances (surpluses) and borrow for emergency response for up to five years of debt service, both without prior voter approval. These have been summarized in VLCT’s 2025 Legislative Wrap-Up.